XI Wiki

XI Wiki

I'm not going to ask my family to pay off my debt. What kind of person do you think I am?

Not to mention the fact that my family doesn't just have that kind of money to loan to me in the first place. If my family had that kind of money laying around, I probably wouldn't have student loan debt to begin with, because they'd be covering my college education.

I'm 33, not 20. My parents aren't responsible for me anymore, nor do I want them to be. Seriously I'm going to put your stupid ass on ignore, because nothing you've said to me in this thread has done anything but aggravate me.

- Navigation

+ Reply to Thread

Results 81 to 100 of 152

Thread: Investment for Noobs

-

2014-09-13 06:12 #81The 69th Donor

Pens win! Pens Win!!! PENS WIN!!!!!

- Join Date

- Mar 2008

- Posts

- 15,106

- BG Level

- 9

- WoW Realm

- Kil'jaeden

-

2014-09-13 06:47 #82If you stopped to actually learn something you might not post these uninformed posts.

- Join Date

- Oct 2006

- Posts

- 1,497

- BG Level

- 6

If your pride is more important then your future then go ahead. But if you don't wanna be 40 with nothing then asking parents for help is not a bad idea. If they can take out a second mortgage with 3% interest which you pay off, you will save yourself $$$ big time.

-

2014-09-13 10:16 #83Special at 11:30 or w/e

Sweaty Dick Punching Enthusiast

- Join Date

- Feb 2012

- Posts

- 10,267

- BG Level

- 9

- FFXIV Character

- Kalmado Espiritu

- FFXIV Server

- Gilgamesh

- FFXI Server

- Sylph

- Blog Entries

- 4

Man he's still going at it! I usually ignore this kind of stuff, but jeez man let it go! No one here wants your advice. No one trusts you or believes in the words you type. Go ahead and think we're all idiots and you are the smart one. It's ok! Just stop!

-

2014-09-13 11:14 #84D. Ring

- Join Date

- Jan 2006

- Posts

- 4,677

- BG Level

- 7

- FFXI Server

- Sylph

While I don't agree with a lot of what this guy says, and while I don't necessarily advocate Aksannyi do this, I actually get part of what he's saying here.If your pride is more important then your future then go ahead. But if you don't wanna be 40 with nothing then asking parents for help is not a bad idea. If they can take out a second mortgage with 3% interest which you pay off, you will save yourself $$$ big time.

There are some parents who have the means and willingness to do this type of thing.

I imagine that many of us posting in this thread do not come from families that would be able or willing to do this, pride aside.

-

2014-09-13 11:48 #85You wouldn't know that though because you've demonstrably never picked up a book nor educated yourself on the matter. Let me guess, overweight housewife?

- Join Date

- Mar 2006

- Posts

- 22,966

- BG Level

- 10

- FFXIV Character

- Allyra Arianos

- FFXIV Server

- Sargatanas

- WoW Realm

- Windrunner

Originally Posted by Aksannyi

Originally Posted by Aksannyi

If you stopped to actually learn something you might not post these uninformed posts. Originally Posted by test123

If you stopped to actually learn something you might not post these uninformed posts. Originally Posted by test123

-

2014-09-13 11:53 #86Black Guy from Predator.

Uppity Negro

Secret Admin

The Immortal Bill Duke

- Join Date

- May 2008

- Posts

- 15,998

- BG Level

- 9

just ban him already and get it overwith, this is stupid

-

2014-09-13 12:02 #87D. Ring

- Join Date

- Jul 2006

- Posts

- 4,961

- BG Level

- 7

- FFXIV Character

- Grey Jorildyn

- FFXIV Server

- Hyperion

Sometimes in life you do have to buck up and do what is in your best interest even if it is difficult. That could be anything at all. Shit I'm 31 and almost moved out years ago because I didn't get along with my parents, then I lost my job, then they got divorced, so I sure am glad I stayed. I didn't leave not because of those things but because I wanted to own a home and avoiding the renting pit. But if I had moved out I would have had a roommate and I hate the idea too, and get it is what I would have had to do if I really wanted to own some day, even if that meant pushing it back a few years or whatever.

If you identify a barrier in life then address it. Being a loner is a thing, I am too, the ultimate introvert if you will, but I work through it. If it goes deeper than a simple "do not want" then find help for it. Life's too short to tell yourself you can't do this or that, especially when there are those out there willing to help.

Some of the advice here is good, some not-so-good. I can hear what test123 is saying but it isn't all relevant to her particular situation. Sometimes you just gotta sit down and prioritize and student loan repayment is just a part of it. Sounds to me like there are other things going on that are privately happening. Unfortunately this is probably not the place you'll find resolutions to those things.

-

2014-09-13 12:14 #88The Shitlord

- Join Date

- Feb 2008

- Posts

- 11,366

- BG Level

- 9

- FFXIV Character

- Kharo Hadakkus

- FFXIV Server

- Hyperion

- FFXI Server

- Sylph

- WoW Realm

- Rivendare

this. it's getting annoying. Originally Posted by Abandon

-

2014-09-13 17:45 #89Chram

- Join Date

- Jun 2006

- Posts

- 2,737

- BG Level

- 7

This is pretty much the most solid investment advice I've seen on a forum. Pretty much exactly what I do as well. Originally Posted by Skirkle

-

2014-09-14 16:05 #90Black Guy from Predator.

Uppity Negro

Secret Admin

The Immortal Bill Duke

- Join Date

- May 2008

- Posts

- 15,998

- BG Level

- 9

dont give me this fucking title if i cant do anything with it

-

2014-09-15 02:43 #91Cerberus

- Join Date

- Sep 2008

- Posts

- 469

- BG Level

- 4

- FFXI Server

- Asura

Also once you pay off a debt that you actively make payments on instead of being wow now i have XXX amount extra to spend a month since you're already used to living without that money put it towards another payment. If the next debt allows it make sure its marked to go towards the principal and it'll pay off the pre-interest amount and you'll end up paying it off sooner and a lower total amount paid. Then just continue snowballing as monthly debts are paid off.

-

2014-09-15 06:36 #92The 69th Donor

Pens win! Pens Win!!! PENS WIN!!!!!

- Join Date

- Mar 2008

- Posts

- 15,106

- BG Level

- 9

- WoW Realm

- Kil'jaeden

Yes, I already have this worked into a spreadsheet I've titled "Two Year Plan." I've already outlined how I'm going to pay down the truck and student loans. If I wanted to get really technical I could break down how all of the loans will be handled individually rather than one big "Sallie Mae" label. Actually I may do that today at work if this shit is slow. (Monday, mid-month, probably.) Originally Posted by Dngnhack

I really do want to pay off the truck loan. Not only am I tying up $250~/month, I've also got a ridiculously high insurance premium thanks to a fucking parking lot fender bender (lady insisted on getting the cops involved, no damage whatsoever but an increase in premium, thanks dumbass). Paying off the truck means I can drop to minimum coverage, which will probably free up about $400/month total with the payment/insurance. And all of that money is going straight to the assholes at Sallie Mae.

I've also laid out how much I need to pay monthly if I want to be debt free in 15 years, 10 years, 5 years. Obviously the goal is 5 years, but realistically, probably not. But seeing the numbers in black and white makes it easy to see what I should be shooting for and to set financial goals for myself.

-

2014-09-15 11:32 #93The Shitlord

- Join Date

- Feb 2008

- Posts

- 11,366

- BG Level

- 9

- FFXIV Character

- Kharo Hadakkus

- FFXIV Server

- Hyperion

- FFXI Server

- Sylph

- WoW Realm

- Rivendare

two year? should make it 5

-

2014-09-15 11:41 #94The 69th Donor

Pens win! Pens Win!!! PENS WIN!!!!!

- Join Date

- Mar 2008

- Posts

- 15,106

- BG Level

- 9

- WoW Realm

- Kil'jaeden

I should, but I was getting hounded by my boss when I made it.

Productive use of company time, you know. lol

-

2014-09-15 12:19 #95The Shitlord

- Join Date

- Feb 2008

- Posts

- 11,366

- BG Level

- 9

- FFXIV Character

- Kharo Hadakkus

- FFXIV Server

- Hyperion

- FFXI Server

- Sylph

- WoW Realm

- Rivendare

5-year plans?! DIRTY COMMIE

-

2014-09-20 22:51 #96Old Merits

- Join Date

- Nov 2009

- Posts

- 1,119

- BG Level

- 6

- FFXI Server

- Fenrir

- WoW Realm

- Kel'Thuzad

Simple philosophy; do you want to work for two weeks now, get nothing from it, in the interest of getting two weeks + 4 hours pay in a year thanks to a low risk CD? If not, watch stocks and buy something, possibly tripling that cash in a year or, likely getting your two weeks pay back per the last two year trend. TDAmeritrade is $10/trade with no maintenance fees. Originally Posted by Aksannyi

If you already have loans out at a fixed rate, determine if the interest paid is less than the possible investment income. You are the loan company's low risk investment.

-

2014-09-22 13:21 #97Un-Rad Conrad

- Join Date

- Oct 2006

- Posts

- 5,043

- BG Level

- 8

- FFXI Server

- Carbuncle

Stocks are for suckers unless you know what you're doing. Index funds are more consistent (less risk and potential earnings of course).

Paying off debt is really the first priority though. Think of it as a no risk, high yield investment since once you pay those funds off, you have that entire loan payment available to you in the future. Pay those off with every available penny you have available. Future You will thank you for it.

-

2014-09-24 06:18 #98D. Ring

- Join Date

- Nov 2006

- Posts

- 4,615

- BG Level

- 7

- FFXI Server

- Quetzalcoatl

- WoW Realm

- Proudmoore

This, first. Originally Posted by galkaindaclub

1. Your basic needs are completely covered.

2. Your short-term, high interest debts are paid, future loans are covered.

3. You've got savings as an emergency funds.

4. Rest goes to the investing.

Best way is to start systematically. Investopedia is a good tool for a beginner. Buy yourself an entry level textbook (don't let the word textbook scare you, intro-levels are quite easy), any good one would do just check the curriculum of your local/national university offering investments class (usually under finance). Studying these is an excellent way to get warmed up until you are financially ready to invest. Get a good book, any edition after the crisis is fine. 2nd hand, etc. should be dirt cheap.

For a more in-depth stock approach, I suggest reading "Stocks for the long run". When it comes to stock investing, always go for the long-run approach, you won't have the tools and connections for an effective day-trading.

Follow wsj.com , forbes.com, marketwatch.com, reuters.com, bloomberg.com, ft.com, businessinsider etc. to get familiar with the language and jargon, as well as increasing your awareness for surrounding economic events and impacts. If you don't have, open a twitter account and follow these.

Reading into your current situation; I'd recommend you not to act too quick with investing. Focus on saving first, that should be your priority. Cut your costs as much as you can, get yourself a job that is stable/or make sure you are in a stable posiition that completely covers your needs, then consider investing. By systematically improving yourself with knowledge, by the time you are financially ready, you will be mentally ready as well.

-

2014-09-24 20:59 #99Ridill

- Join Date

- May 2005

- Posts

- 13,568

- BG Level

- 9

Ruke is correct here. Originally Posted by RKenshin

If you actually crunch the numbers, you can rent a home and invest the "nest egg" you'd otherwise put down as a down-payment, save on paying interest towards on a mortgage, and in the long run you end up doing just as well as if you owned property.

-

2014-09-24 22:59 #100Groinlonger

- Join Date

- Oct 2006

- Posts

- 2,964

- BG Level

- 7

- FFXI Server

- Fenrir

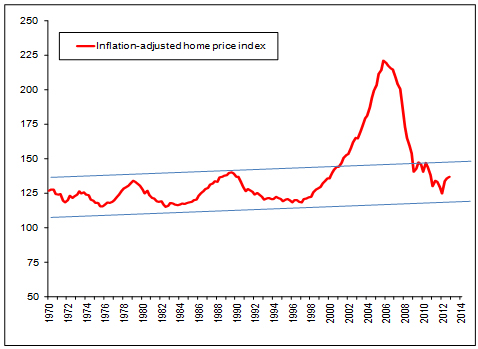

Not exactly. A mortgage payment is lower than renting for the same house. Maintenance and taxes offset that cost to be about the same. The advantage is that some of your monthly living expenses are recovered in the form of equity. It can truly pay off in the long run when you consider your monthly payment is set in stone (i.e. won't be affected by inflation.) and that every month more of your monthly living expenses are recovered. You don't need a huge down payment for all loans either. The S&P index is an invalid comparison unless you're squatting somewhere and can invest all of the money you'd otherwise spend on a mortgage payment. test's logic is totally flawed although buying a home can be still be a good financial decision. It can also be a terribly bad idea though.

Reply With Quote

Reply With Quote

Similar Threads

-

Chuckie says farewell for awhile.

By Chuckie in forum General DiscussionReplies: 7Last Post: 2004-07-22, 11:35