XI Wiki

XI Wiki

Okay I didn't want to necro other credit score-related threads cause none were that recent or related.

I had (maybe still have) minimal credit history. Student loans apparently didn't really count, no credit card (approved and one arriving soon), no car loans, mortgage, etc.

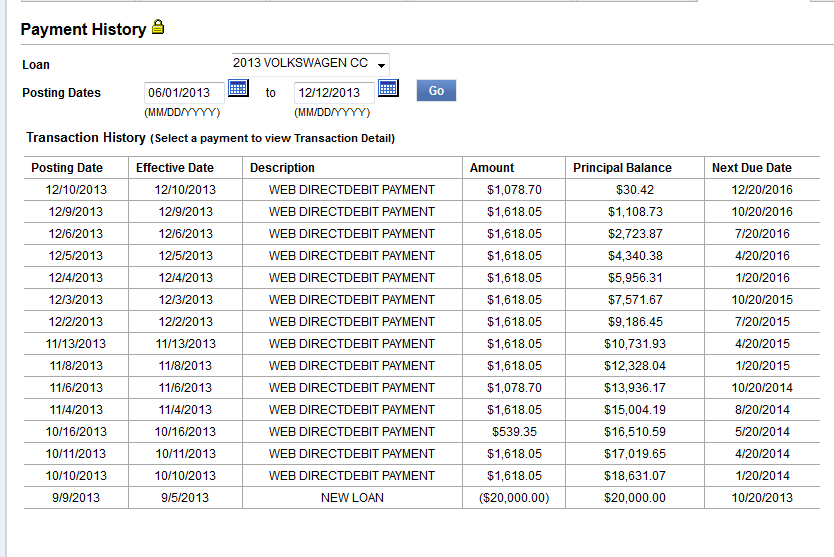

So I finance 20k on car. They come back with not low credit but no credit. Terminology in their report was 'not enough history to generate a credit score' or something similar. So I get shit financing (13% lol). This loan was effective Sept 5th, 2013.

I kinda said f that to the garbage interest rate, so I widdled the principal down as quickly as possible. My question is how long should I keep this line of credit open/active? Isn't that a big factor in evaluating credit worthiness? Should I keep it open 6 months, a year, 2 years? The principal balance is now like 30 bucks, so I'm not really fretting 13% interest on that for awhile. I just want to maximize however possible the benefit from this line of credit. When the credit card arrives (3k limit), I'll try to use a thousand or two early on and then only use like 10-25% of the limit.

payment history to-date on loan in question

Spoiler: show

- Navigation

Results 1 to 18 of 18

-

2013-12-12 10:28 #1

Sweaty Dick Punching Enthusiast

- Join Date

- May 2005

- Posts

- 9,143

- BG Level

- 8

- FFXI Server

- Fenrir

Credit Reporting and History -- Length of Loan

-

2013-12-12 10:36 #2Wild Card

- Join Date

- Aug 2012

- Posts

- 2,805

- BG Level

- 7

- FFXIV Character

- Mina Pulchra

- FFXIV Server

- Gilgamesh

- FFXI Server

- Lakshmi

- WoW Realm

- Hyjal

- Blog Entries

- 16

If anyone could nail down the exact equation for the three bureaus for you I would love to have a copy of it.

General rule of thumb is the longer the history you show the better it looks on your credit report. I have a credit card line that has been open since the day I turned 18. I pay gas with that card to this day on it. I recommend this method to a lot of people starting out because most credit cards start with a very low credit line and gas is something that you can regularly pay for and pay off on a monthly basis to show continuous history.

So if you want to improve your credit score you should try to drag out the payment as long as possible.

-

2013-12-12 10:39 #3

SASSAGE KING OF DA WORLD

cheap hawks gay

- Join Date

- Sep 2007

- Posts

- 26,424

- BG Level

- 10

13% would be a dream for me lol, I'm going to get hit with like 30%+ because of defaulted student loans when I try to get a car next year.

-

2013-12-12 10:40 #4Wild Card

- Join Date

- Aug 2012

- Posts

- 2,805

- BG Level

- 7

- FFXIV Character

- Mina Pulchra

- FFXIV Server

- Gilgamesh

- FFXI Server

- Lakshmi

- WoW Realm

- Hyjal

- Blog Entries

- 16

I'm at a loss for words. Originally Posted by Callisto

Originally Posted by Callisto

I'm 3% on my Jeep. I was not aware 30% was actually a thing they could do. Fucking student loans...

-

2013-12-12 10:42 #5

SASSAGE KING OF DA WORLD

cheap hawks gay

- Join Date

- Sep 2007

- Posts

- 26,424

- BG Level

- 10

It was a slight exaggeration but I know my g/f was quoted above 20 without a co-signer when she had to replace her car, and she definitely has better credit than I do.

-

2013-12-12 11:28 #6Ruke

- Join Date

- Nov 2005

- Posts

- 3,972

- BG Level

- 7

My understanding of the credit score calculation:

There are two different types of debt, and they are scored and affect your score differently.

Credit cards are categorized as revolving debt, and show how well you can control your spending and manage your finances over time… particularly with access to what can often be large sums of money when you combine credit limits across multiple cards. Maintaining a low overall balance (<20%), across 2-4 cards, with a high amount of credit available (comes with time), on-time payments, etc will make up the bulk of your actual credit score. This is why you can have a crap credit score, despite having student loans and car loans. Bad management of credit card debt often translates into bad management of other forms of debt.

Note that the <20% balance refers to your overall combined credit limit. If you have 2 cards with a $1000 limit, you could have one card with $400 and the other card with $0 and be OK. Though, avoid going over more than 60% on any one card, regardless.

Student loans, car loans, and mortgages are classified as installment debt. Payment history matters more here, as it shows that you can take on what are typically higher debt obligations and manage your finances to pay them in a timely, reliable manner. Whatever you do, don’t miss a payment (for both revolving and installment debt, but especially installment).

Mortages can also double dip in your history as both an installment debt and a revolving debt, because with a mortgage comes access to equity and loans against your home value.

-

2013-12-12 14:54 #7

Sweaty Dick Punching Enthusiast

- Join Date

- May 2005

- Posts

- 9,143

- BG Level

- 8

- FFXI Server

- Fenrir

Helpful info, thanks for replies. My mistake the last 10 years has been having no revolving debt history at all. I will keep the loan in Repayment at least through a few months of credit card history.

It's weird; you're told kinda an absolute 'stay away from credit cards' when one's younger. When really that's something you should get going asap, albeit with proper discipline.

-

2013-12-12 15:03 #8Wild Card

- Join Date

- Aug 2012

- Posts

- 2,805

- BG Level

- 7

- FFXIV Character

- Mina Pulchra

- FFXIV Server

- Gilgamesh

- FFXI Server

- Lakshmi

- WoW Realm

- Hyjal

- Blog Entries

- 16

I used to work with a bunch of guys at an airline maintenance base. They had two favorite topics.

1. Their wives

2. Their credit debt

I was 18 at the time and they were always telling me how credit cards ruined their lives and that I should never get one. Totally ignored all their advice and got a credit card. Just be responsible with it and treat it like the cash you actually have and not amount it is worth.

-

2013-12-12 15:34 #9I Am, Who I Am.

- Join Date

- Nov 2005

- Posts

- 15,656

- BG Level

- 9

- FFXIV Character

- Trixi Sephyuyx

- FFXIV Server

- Excalibur

- FFXI Server

- Ragnarok

I've heard this "keep debt on CC" thing both ways for years, and I think it's BS. CC has been my only source of "debt" since I was 18ish; I've never had a loan up to the point of purchasing a house. Everything else I've purchased is paid in full, mostly in the form of paying off my CC every month in full (get rewards for putting stuff on CC, so why not?). Originally Posted by RKenshin

In any case, I have a high/perfect credit score and my only form of credit is a long standing CC (only one CC) with a high limit, and low interest rate that I pay off every month.

Banks just want you to think your credit is better with a little bit of CC debt so that they can get some free monies.

-

2013-12-12 15:59 #10E. Body

- Join Date

- Dec 2006

- Posts

- 2,332

- BG Level

- 7

RKenshin is correct in regards to how the score is calculated.

That being said, keeping any balance on a card for the sheer point of raising your credit score is not the right thing to do and it's effects on your score are greatly exagerrated. It does increase the score slightly to have that debt against you, but quite honestly it does not affect the score all that much.

What's important is the advice Seph mentioned above. Use the credit you are applying for. If you apply and receive a credit card with a $500 or $1000 limit, use it for every day purchases and pay everything off at the end of the month. After a couple years you'll have access to some really good interest rates and some great credit card offers. The highest FICO score you can have is an 850. I hit that 3 years ago when I purchased my house (mortgage), I'm 29 for reference.

I laugh when people say how evil credit cards are. They are only evil for people who cannot manage money. Credit cards are fucking awesome once you establish your credit. Long interest free period on balance transfers with very low fees (1-2% in some cases), points, etc. You can have access to all of that without it bankrupting you. One of my favorite things to due is use my points card, then hit the balance offer afterwards if it's a big purchase. Goes kind of like this (bare with me here):

Amazon Visa. I get 3 points for every $1 spent at Amazon. 100 Points = $1. Roughly 3% return is how it works out.

So I buy purchased some electronics on Amazon in January for roughly $1700. I received 5100 points, equating to $51.00

Now at right at the end of January I paid 1/2 of the balance. Leaving me with an owed balance of $850. Now before the bill was actually due, I transferred the balance to my Discover Card. 2% Fee for Balance Transfer and 0% APR for 12 Months. That allows me to push out the payment of that final $850 up to 18 months, for the additional price of $17.

Now keep in mind I MADE $51.00 just buying the shit in the first place. So Net, I am up $34.00. and the remaining $850 I have 18 months to pay off at 0% interest.

I'm sure you can see where juggling and managing your points and offers can help out a lot in times when you are stuck making a surprise large purchase, or something along those lines.

-

2013-12-12 16:38 #11FOR FUCKS' SAKE !!!

FOR FUCKS' SAKE !!!

FUCK FUCK FUCK

- Join Date

- Mar 2010

- Posts

- 14,680

- BG Level

- 9

Yeah, not sure why people kept saying to never get a credit card. I got one when I was 18 and now my scores over 800. Financed two cars and two motorcycles no problem and according to my mortgage broker friend, should have absolutely no problem shopping around for some of the better rates.

-

2013-12-12 20:42 #12Ruke

- Join Date

- Nov 2005

- Posts

- 3,972

- BG Level

- 7

I think you may have misread; I didn't say that carrying a CC balance is good for your score (nor did I recommend it). I said that you had to ensure that your balances remain (whatever they are) <20% of your total limit, and that the account stays open, and is paid on time. Originally Posted by SephYuyX

I never carry an actual balance month-to-month either, and I'm somewhere in the high 700s (or I was ~2 years ago, I'd imagine I'm higher now).

I too use and recommend using a credit card for every day purchases, if you have the self-control, and then pay it off at the end of the month. The cash-back rewards add-up nicely. I get an extra $250-400 worth of cash back bonuses accrued each year, and use it to buy myself some nice stuffs around x-mas time.

Also, it's worth noting that in most cases you legally can't be charged interest on any purchases you make in the current statement period, until the next statement period ends.

IE: I buy $1,000 worth of stuff in the statement period May 1st - June 1st, June 1st being the day the statement ends and closes. I won't be charged interest on that $1,000 so long as I pay it off by the end of the next statement period, which at one month later would give me until July 1st.

-

2013-12-13 09:55 #13E. Body

- Join Date

- Dec 2006

- Posts

- 2,332

- BG Level

- 7

Just got an offer in the mail for a new Citi Card. 2 years interest free on first month of purchases if I sign up.

Hmm.....

-

2013-12-13 11:26 #14If you stopped to actually learn something you might not post these uninformed posts.

- Join Date

- Oct 2006

- Posts

- 1,493

- BG Level

- 6

drive crap until you can cash out a newer one.

-

2013-12-13 11:37 #15RNGesus

Sweaty Dick Punching Enthusiast

- Join Date

- Jan 2005

- Posts

- 42,982

- BG Level

- 10

- FFXIV Character

- Lenette Valkyr

- FFXIV Server

- Gilgamesh

Originally Posted by Callisto

Yeah I can't even imagine that @_@ Mines 2.49% Originally Posted by Mina

And even with that I've been wondering the same thing, whether or not I should just pay it all off or keep the line open for a while to build credit.

I thought the keeping the debt just meant the monthly shit until you pay it off. As far as my credit is concerned I have some amount on my CC at all times but it's always paid off in a timely manner every month. Originally Posted by SephYuyX

-

2013-12-13 13:54 #16

Sweaty Dick Punching Enthusiast

- Join Date

- May 2005

- Posts

- 9,143

- BG Level

- 8

- FFXI Server

- Fenrir

Finance dude at dealership said keep it up open at least 6 months, not sure if you've already reached that length. I'll wait til March or so to pay this off I think. I don't get the title while it's in Repayment obviously, but that's not a big deal to me right now. Originally Posted by Tyrath

-

2013-12-13 15:13 #17RNGesus

Sweaty Dick Punching Enthusiast

- Join Date

- Jan 2005

- Posts

- 42,982

- BG Level

- 10

- FFXIV Character

- Lenette Valkyr

- FFXIV Server

- Gilgamesh

Well when I got the car I basically had no credit history. I got a later start on having credit cards and whatnot. My dad co-signed it so the guy told me I should do at least 2-3 years to get going on some credit building. I'll hit 2 years in april. I wasn't sure though if his advice was actually for my benefit or if he just wanted me paying interest longer. Originally Posted by Roranora

At this point my credits gotten up to the mid 700s. The average length of all my accounts ends up only being 11 months so I'm worried that closing the car loan will lower that even more.

-

2013-12-13 15:31 #18

Sweaty Dick Punching Enthusiast

- Join Date

- May 2005

- Posts

- 9,143

- BG Level

- 8

- FFXI Server

- Fenrir

Shit, the average length of my installment loans is crappy too, maybe 1-2 years only. I only have a $3000 loan from a small bank in 2009, paid off in ~7 months, and ~50k student loans, which I guess all vary in length from the time they were first distributed back in 2004 up to some in 2009. They were paid off in Feb 2012, so maybe I have some 5+ year installment lengths, not sure. It'd be 22 months at the very least, from graduation to repaying. And that bullshit was only good enough to get me a very unimpressive 13% interest rate on this loan. I only had one lender even willing to deal with me, too. (Wells Fargo)

Now add the car loan to it - 3 installment loans in my life. It seems to me that is both a nice middle ground between no history at all and tons of recklessly managed credit. I'm just salty about getting 13% and only 1 lender, but it's good I learned the lesson now. I hope to someday get a business loan and maybe a mortgage with much better interest rates; thus this thread.. along with other researching into how this credit jibberish works.

Hopefully this credit card helps out quickly, and I'm deemed more credit worthy in a year or two. And on that topic, I think it's being sent via horseback. Instant approval, it'll be there 'in 7-10 business days!', a week goes by, email get, says shipped yesterday and will now be there in 2-3 weeks.

Similar Threads

-

List of the top selling computer and video games of all time

By spaghetti_monster in forum General DiscussionReplies: 17Last Post: 2006-10-09, 08:24 -

Net Neutrality and the future of the internet

By Illverin in forum General DiscussionReplies: 8Last Post: 2006-07-21, 03:10 -

Harry Potter and the Goblet of Fire

By Warudo Ecksu in forum General DiscussionReplies: 57Last Post: 2005-11-25, 16:22 -

Free Credit Reports

By Endo in forum General DiscussionReplies: 1Last Post: 2005-08-29, 13:34